by AdvisorAnalyst.com in collaboration with AGF Capital Partners

Navigating Volatility:

The Case for Tactical Alpha

by AdvisorAnalyst.com in collaboration with Franklin Templeton Investments

Bridging the Gap Between Safety and Return

How Franklin Templeton’s Brian Calder is Redefining Cash Management

The Cash Conundrum

For many investors, 2025 has felt like a test of patience and conviction. Cash feels safe—but safety has a cost. In a world where “higher for longer” interest rate expectations meet volatile bond markets and stretched equity valuations, portfolios heavy in cash are quietly underperforming.

“It’s a paradox,” notes Pierre Daillie in AdvisorAnalyst’s in-depth conversation with Brian Calder, Vice President, Portfolio Manager and Senior Bond Trader at Franklin Templeton Fixed Income, for this article. “On one hand, cash feels prudent—dry powder. On the other, sitting idle in a checking account that earns next to nothing, or in a sweep vehicle, which at best, earns a negative real return—that erodes purchasing power.”

Calder, who co-manages the Franklin Canadian Ultra-Short Term Bond Fund (and it's ETF series FHIS) alongside the firm’s other flagship fixed income mandates, has spent more than two decades navigating precisely this intersection—where liquidity meets opportunity. His perspective reflects both the trader’s instinct and the portfolio manager’s discipline: “After years of near-zero rates, investors are rediscovering that cash can actually work again,” he says. “The question is how to make it work efficiently—without losing the security and flexibility investors value most.”

From Idle Cash to Active Strategy

The behavioural shift, Calder observes, has been gradual but clear. “Investors have become more sophisticated and more aware of the drag that cash can apply to portfolios,” he explains. “They want to make sure that every dollar contributes to the overall return, without giving up safety or liquidity.”

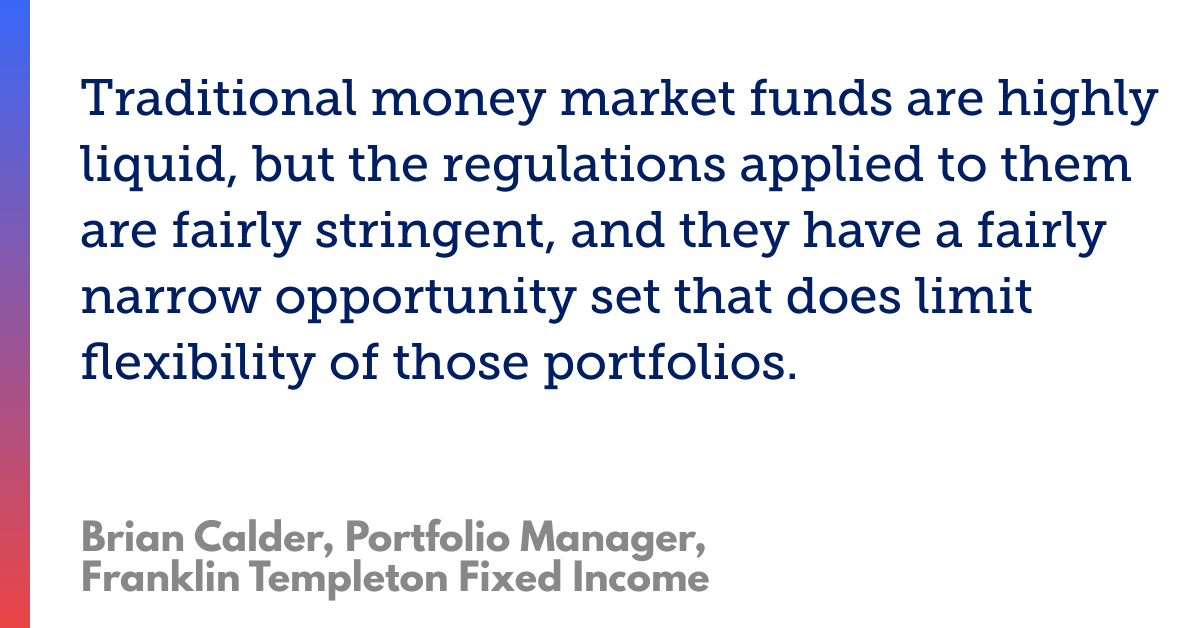

The old toolkit—GICs, high-interest savings accounts, and money market funds—no longer satisfies that balance. GICs lock up capital and penalize early withdrawals; savings accounts have seen yields trimmed by regulatory changes; and money market funds, though highly liquid, are constrained by rules that limit both term and credit exposure.

“The result,” says Calder, “is a narrow opportunity set. Money market products are bound to the very short end of the curve—30, 60, 90-day paper. That limits their flexibility and their yield. Ultra-short bond strategies, by contrast, give you the freedom to move slightly further out the curve, to capture opportunities while keeping rate exposure very low.”

Why is it time to rethink positioning of short term liquid assets?

What's your approach and view to ultra-short bond investing?

Two Ways to Access the Strategy

The partnership via AGF Capital Partners offers two ways to access private credit:

- AGF SAF Private Credit Limited Partnership (LP): a pure-play structure with 100% exposure to private debt, designed for institutions and sophisticated investors comfortable with illiquidity.

- AGF SAF Private Credit Trust: tailored for investors seeking the ballast of private credit but with a liquidity sleeve, and lower minimum investments. Holding 10–15% in liquid assets, it’s built for those who need flexibility.

“Both vehicles have the same underlying portfolio,” Lawrence clarifies. “It’s just a matter of deciding on fit.”

Why 'cash' positions should be considered a contributor to total return.

How does scale, depth of research, and active management provide an edge?

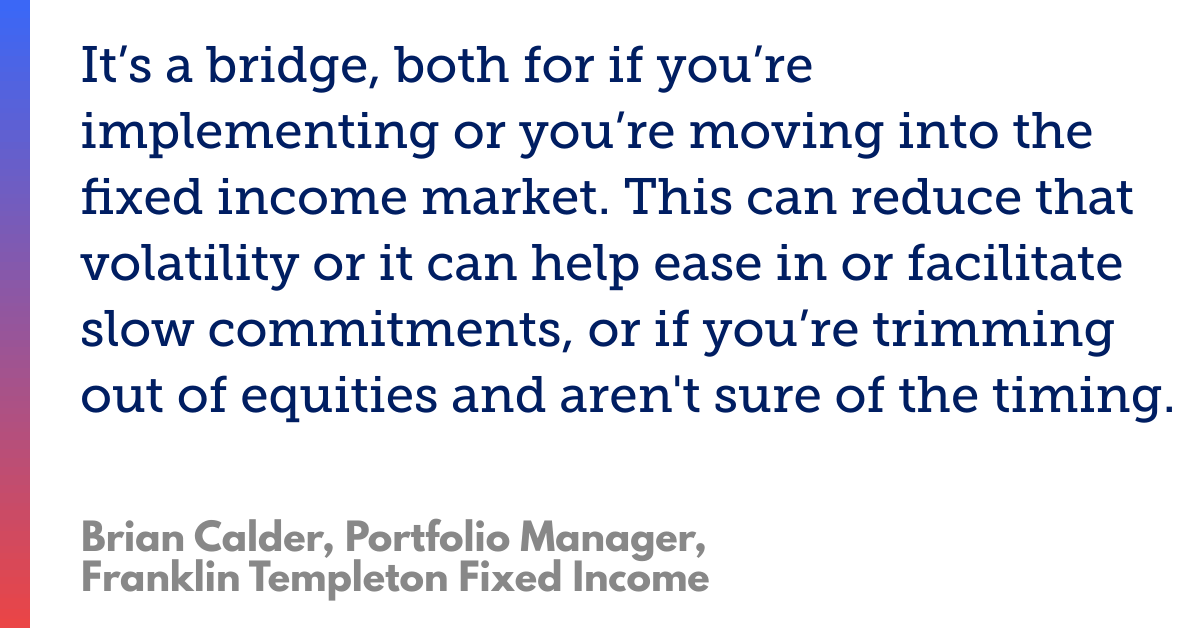

How can the ultra-short bond strategy bridge transitions to longer-term investment decisions?

How do the various cash equivalents compare to ultra-short strategies?

What “Ultra-Short” Really Means

Ultra-short bond strategies like FHIS occupy a unique niche—sitting between the traditional money market and short-term bond categories. Calder describes it as “the part of the curve that offers the greatest flexibility.”

“Ultra-short strategies typically operate within a window of about two-thirds to three-quarters of a year in duration,” he explains. “That’s been the sweet spot for us—long enough to earn a meaningful yield, short enough to avoid excessive volatility. Investors don’t want a roller coaster.”

The approach is designed to seize opportunities that are “a little too long” for money market mandates, yet “far less volatile” than conventional short-term bonds. That middle ground, Calder explains, “fills the gap in the fixed income spectrum—helping portfolios stay productive while maintaining liquidity.”

The Active Edge

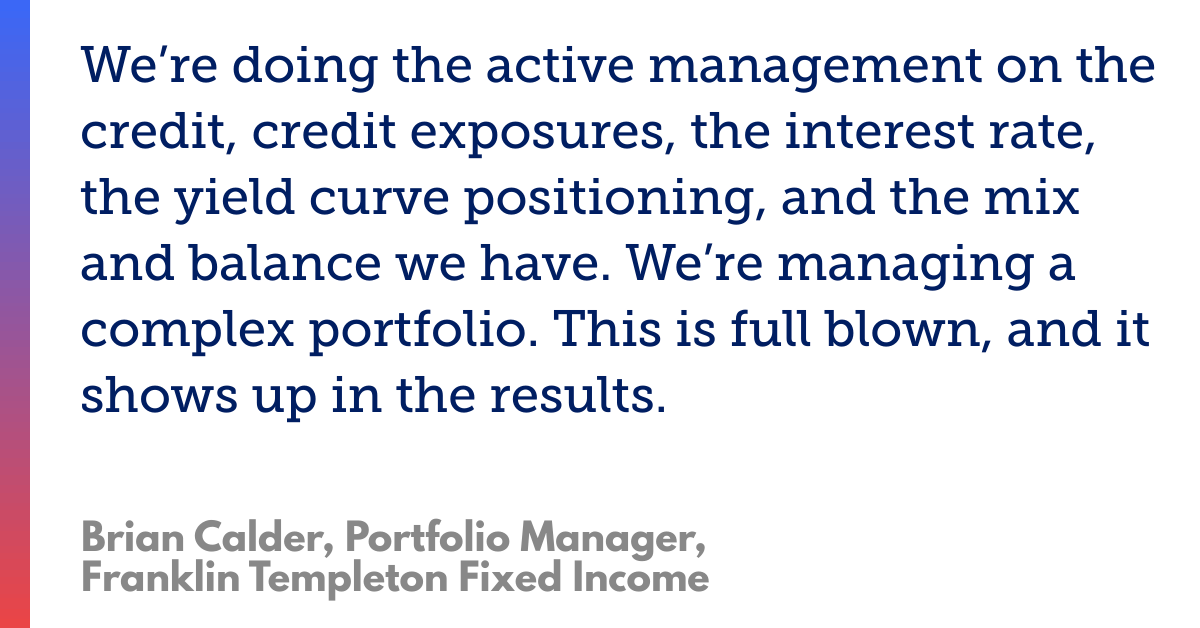

What sets FHIS apart isn’t just its position on the curve—it’s how actively it’s managed. Calder’s team leverages the scale and depth of Franklin Templeton’s global fixed income platform, executing trades daily across dozens of issuers.

“The bond market is an over-the-counter market,” Calder explains. “It’s not as visible to the retail investor, and efficiency depends on scale. We’re building portfolios of over a hundred positions, benefiting from institutional pricing that’s simply not accessible to individual investors.”

Equally important is the credit work behind those trades. “We rely heavily on our in-house credit analysts,” he says. “They know these companies inside and out. The last place I want to learn about something is in a rating agency report,” he emphasizes. “By then it’s too late. Our goal is to identify opportunities before they hit the public radar.”

That combination of proximity to the market and proprietary research gives FHIS an agility most passive vehicles lack. “It’s not a simple T-bill fund,” Calder emphasizes. “We’re managing exposure to corporates, government paper, even a modest high-yield allocation—all within a disciplined framework. The complexity shows up in the results.”

Built for All Seasons

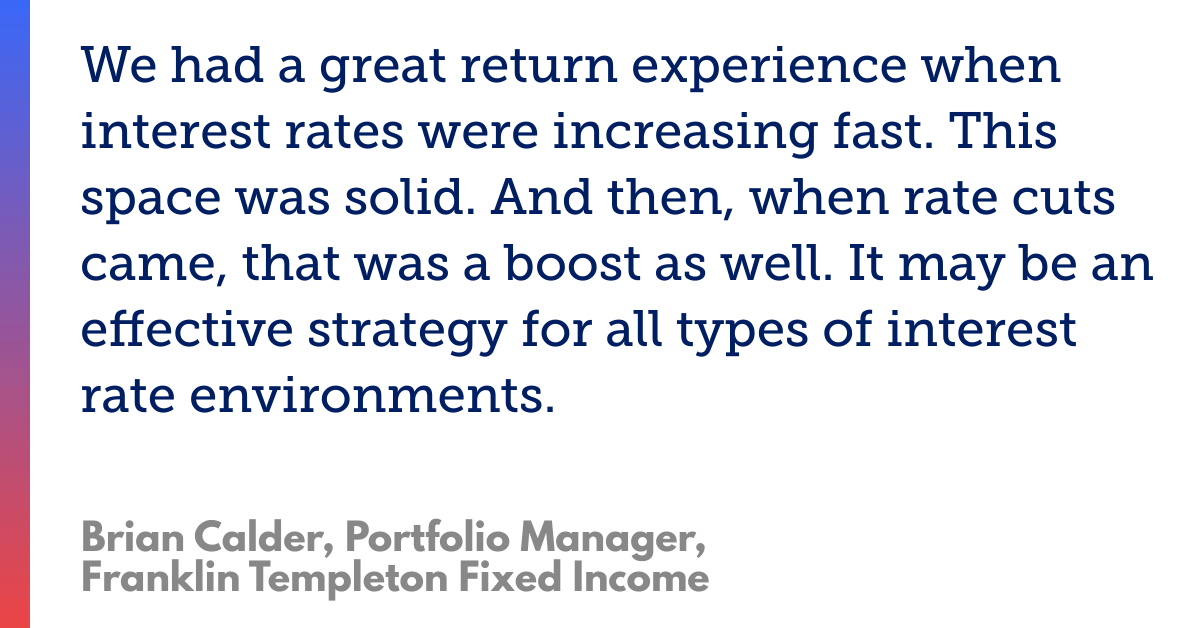

One of the strategy’s under-appreciated strengths is its resilience across rate cycles. “When we launched FHIS, policy rates were still near zero,” Calder recalls. “People wondered why anyone would care. But when rates started rising, the strategy performed exceptionally well. And now, as rates begin to ease, it’s benefitting again.”

That resilience comes from its focus on the “front end of the curve”—the zone least sensitive to large rate swings. Calder puts it simply: “We’ve seen great returns when rates were rising rapidly, and now we’re seeing another tailwind as they come down.”

Real Yield, Real Flexibility

FHIS is designed to function as a strategic fixed income holding—pursuing higher yields with minimal volatility. For some advisors, it’s used as a volatility reducer, paired with longer-duration bond funds to smooth portfolio performance.

“It works beautifully as a transition vehicle,” Calder notes. “If you’re trimming equities but not ready to commit to longer-term bonds, FHIS lets you stay invested, pursue a healthy yield, and retain daily liquidity. And if you’re managing withdrawals or de-risking a portfolio, it lets you shorten duration without giving up income.”

The fund’s duration target of less than a year and its daily liquidity make it an adaptable building block. “It reduces cash drag,” Calder says. “You’re putting your liquidity to work while maintaining access. That’s exactly what investors want in uncertain times.”

Making Cash Count

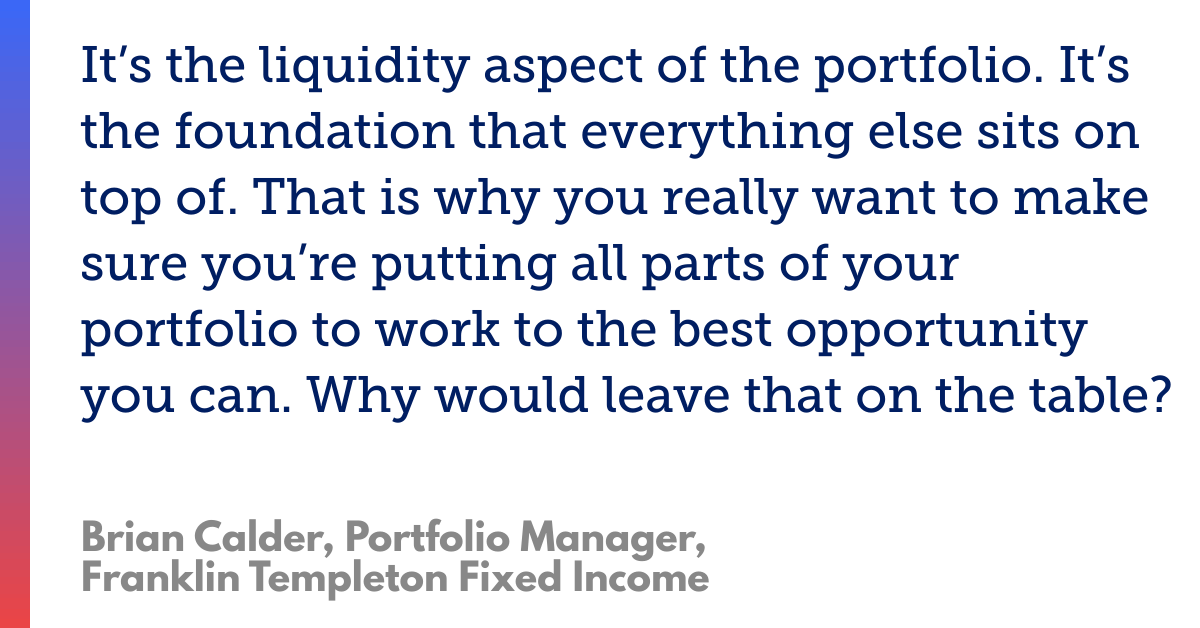

To Calder, the conversation about cash is ultimately about opportunity cost. “Holding cash that doesn’t keep up with inflation means losing purchasing power—that’s suboptimal,” he says. “Why would you leave that [income] on the table? Every part of the portfolio should be contributing to return.”

That philosophy aligns with a broader shift in advisor behaviour. “Advisors are scrutinizing their cash instruments more closely now,” he adds. “They’re demanding the same level of due diligence they would apply to any other part of the portfolio.’ It’s part of the total return equation.”

And the data supports his enthusiasm. The fund’s net asset value has been steadily climbing, supported by consistent monthly distributions—a sign of both underlying stability and active income generation.

“You’re getting the best of both worlds,” Daillie observes. “Regular payouts, and a real return on your liquid assets.”

Calder agrees: “It’s a simple idea that takes a lot of work behind the scenes. But the outcome speaks for itself.”

Why It Matters

Beyond the portfolio math lies a broader behavioural truth: investors often underestimate the strategic role of cash. “We tend to think of cash as inert,” Calder says. “But it’s actually the foundation—the stability layer everything else rests on. You want that layer to be as productive as possible.” And accessible, when opportunity strikes.

For advisors, this reframing has major implications. FHIS isn’t just a placeholder—it’s an upgrade. It helps advisors keep client capital engaged, pursuing a positive real return while maintaining flexibility for future opportunities.

In an environment defined by uncertainty—economic, political, and market-related—that balance of safety and productivity may be the ultimate competitive advantage.

From Passive Cash to Active Opportunity

Calder reflects on the changing perception of fixed income. “Fixed income used to be considered boring,” he laughs. “But the reality is, it’s where a lot of the [market’s] brainpower lives. The opportunities are dynamic, the pace is fast, and active management makes all the difference.”

In a market still searching for equilibrium between risk and restraint, the Franklin Canadian Ultra-Short Bond Fund (FHIS) stands out as a versatile tool for both. It pursues a real return, and a strategic fixed income anchor that tempers volatility without compromising liquidity.

For advisors and investors navigating the “in-between” phase—waiting for clarity on rates, valuations, or market direction—Calder’s message is clear:

“Every part of your portfolio should be working. Your liquid assets don’t have to sit idle. With the right strategy, they can remain accessible while earning a meaningful return.

What's the investor experience been like in the ultra-short bond strategy?

Why the ultra-short strategy makes sense in this period of rates uncertainty?

Every basis point counts. Liquid assets should be made as productive as possible.

Key Takeaways

As markets shift, advisors need to adapt their tools and strategies. Here are the main insights from the discussion:

- Cash Is No Longer Passive - In today’s “higher for longer” environment, excess cash is a silent performance drag. Calder emphasizes that cash should be treated as an active, strategic asset—not idle capital.

- Ultra-Short Bonds Fill the Gap - The Franklin Canadian Ultra-Short Bond Fund (FHIS) bridges the gap between money markets and short-term bonds, offering meaningful yield potential while maintaining liquidity and low volatility.

- Active Management Adds Value - Calder’s team leverages Franklin Templeton’s institutional scale and in-house credit research to identify opportunities early and optimize yield—advantages unavailable in passive or retail cash vehicles.

- Adaptability Across Rate Cycles - FHIS has shown resilience whether rates rise or fall, due to its focus on the “front end of the curve.” It’s designed to capture returns without exposing investors to large rate swings.

- A Strategic Tool for Portfolios in Transition - Advisors can use FHIS to reduce cash drag, manage de-risking phases, or park assets between equity and longer-term bond allocations—keeping client portfolios productive, flexible, and ready for opportunity.

Brian Calder

Portfolio Manager, Senior Bond Trader

Brian Calder is a vice president, portfolio manager and senior trader for Franklin Templeton Fixed Income. Mr. Calder is responsible for co-leading management of Franklin Canadian Government Bond Fund, Franklin Canadian Bond Fund, Franklin Canadian Balanced Fund, Franklin Canadian Ultra Short-Term Bond, and the Franklin Canadian Fixed Income and Balanced SMA strategies. In addition, Mr. Calder is also responsible for the management of a number of institutional accounts. He also performs analysis on federal, provincial and municipal issuers, and is the lead trader for the Franklin Templeton Canadian Fixed Income team.

Mr. Calder joined Franklin Templeton in 2001 and has over 24 years of experience in the financial services industry. Prior to Franklin Templeton, Mr. Calder held a client facing role with another Canadian asset manager.

Mr. Calder holds a degree in Economics from the University of Calgary and also the Chartered Investment Manager (CIM) designation.

Meet Ash Lawrence, AGF Capital Partners

Ash Lawrence is Head of AGF Capital Partners, AGF Management Limited’s diversified alternatives business, and a member of AGF’s Executive Management Team. With over 20 years of expertise in alternative investments and portfolio management, Ash leads initiatives to expand AGF’s private asset and alternative strategy capabilities.His team partners with experienced investment managers, providing strategic support, resources, and capital to foster growth and innovation. Before joining AGF, Ash spent 16 years at Brookfield Asset Management, where he led Canadian real estate investments and managed portfolios across North America and Brazil. Ash holds an MBA from the Rotman School of Management and a Bachelor of Applied Science in Civil Engineering from the University of Waterloo. He serves on multiple boards and is a Global Governing Trustee for the Urban Land Institute. Ash’s early career includes financing municipal infrastructure and developing solutions for public and private sectors.

Ash Lawrence

Head of AGF Capital Partners

Navigating Volatility:

The Case for Tactical Alpha

by AdvisorAnalyst.com in partnership with AGF Capital Partners

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla.

Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum. Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi u t aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla.

Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum. Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi u t aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

Lorem ipsum dolor sit amet, consectetur

Lorem ipsum dolor sit amet, consectetur

In an era of economic flux and market volatility, alternative investments have emerged as a cornerstone of portfolio construction, offering the potential for diversification, resilience, and enhanced returns. Yet, navigating this terrain requires expertise and a nuanced understanding of its complexities. Ash Lawrence, Head of AGF Capital Partners, and Scott Radke, CEO and Co-CIO at New Holland Capital, share their thoughts on the landscape, the recent launch of AGF NHC Tactical Alpha Fund and how to navigate alternatives strategies.

"We might see a different return

environment for public equities,"

Lawrence observes.

Meet Scott Radke, New Holland Capital

Scott Radke is the Chief Executive Officer and Co-Chief Investment Officer at New Holland Capital (NHC). As CEO, Scott is responsible for leading, implementing, and growing NHC’s business activities. As Co-CIO, Scott is responsible for portfolio management, investment research, and portfolio risk alongside David Wadler with a special focus on illiquid strategies, and Bill Young with a special focus on liquid strategies. Scott is a member of the firm’s Financial Risk Management Committee and a member of the Investment Committee, which opines on investment and portfolio decisions across NHC’s business lines. Prior to the launch of NHC in 2006, Scott was a member of the Hedge Fund Group within a Dutch pension. Before that, Scott was a Vice President at Citigroup Global Markets and previously an Associate within the Insurance-related Structured Transactions Group at Goldman Sachs. Scott graduated magna cum laude from the University of Michigan with a BSE in Mechanical Engineering and received an MBA in Finance with distinction from the Wharton School of the University of Pennsylvania.

Scott Radke

CEO & Co-CIO, New Holland Capital

The State of the Market: A Catalyst for Change

“We might see a different return environment for public equities,” Lawrence observes, pointing to post-GFC monetary stimulus as a bygone era. The days of easy gains and low volatility are over. With public equity returns concentrated in a few high-performing sectors, diversification is critical.

The challenge lies in reallocating portfolios to capture these opportunities while mitigating risk. “How do I reallocate for the future?” Lawrence asks rhetorically. The answer lies in alternatives, which offer a way to diversify and buffer against public market downturns.

"We might see a different return

environment for public equities,"

Lawrence observes.

About Ash Lawrence, AGF Capital Partners

Ash Lawrence is Head of AGF Capital Partners, AGF Management Limited’s diversified alternatives business, and a member of AGF’s Executive Management Team. With over 20 years of expertise in alternative investments and portfolio management, Ash leads initiatives to expand AGF’s private asset and alternative strategy capabilities.His team partners with experienced investment managers, providing strategic support, resources, and capital to foster growth and innovation. Before joining AGF, Ash spent 16 years at Brookfield Asset Management, where he led Canadian real estate investments and managed portfolios across North America and Brazil. Ash holds an MBA from the Rotman School of Management and a Bachelor of Applied Science in Civil Engineering from the University of Waterloo. He serves on multiple boards and is a Global Governing Trustee for the Urban Land Institute. Ash’s early career includes financing municipal infrastructure and developing solutions for public and private sectors.

About Scott Radke, New Holland Capital

Scott Radke is the Chief Executive Officer and Co-Chief Investment Officer at New Holland Capital (NHC). As CEO, Scott is responsible for leading, implementing, and growing NHC’s business activities. As Co-CIO, Scott is responsible for portfolio management, investment research, and portfolio risk alongside David Wadler with a special focus on illiquid strategies, and Bill Young with a special focus on liquid strategies. Scott is a member of the firm’s Financial Risk Management Committee and a member of the Investment Committee, which opines on investment and portfolio decisions across NHC’s business lines. Prior to the launch of NHC in 2006, Scott was a member of the Hedge Fund Group within a Dutch pension. Before that, Scott was a Vice President at Citigroup Global Markets and previously an Associate within the Insurance-related Structured Transactions Group at Goldman Sachs. Scott graduated magna cum laude from the University of Michigan with a BSE in Mechanical Engineering and received an MBA in Finance with distinction from the Wharton School of the University of Pennsylvania.

Diversification is critical–but what kind?

Ash Lawrence talks about the kind of diversification needed in the current investment environment, and how investors can begin to think about how to thoughtfully diversify and buffer investment portfolios.

Ash Lawrence: There is generally a view that in the mid to long term looking forward, we might see a different return environment for public equities versus looking backwards for that same five- to ten-year period. We may, for the near term, you know, election results in the U. S. and some other things, see a bull run continue.

But I think generally no one is expecting the rate environment and monetary stimulus environment to return that we saw in the almost decade after the GFC. And I think in that context, when coupled with some of the concentration that you're seeing in the public markets and where that return attribution is coming from, it's not really a broadly diversified high performing public equities market right now. It's quite narrow in terms of where the returns are coming. Again. What you alluded to at the beginning, um, starting for for investors to start to think about how do I reallocate for the future, my, you know, maybe it's a basic 60 40–we'll just start with that assumption.

How do I reallocate for the future if that's my expectations on public equity returns? How do I get that diversification? And if I do think public equity returns are going to moderate to some degree over the long term, how do I reallocate so I'm not just mimicking that, in another asset class, which again, the sort of lower correlation asset classes, that's sort of the environment we think about.

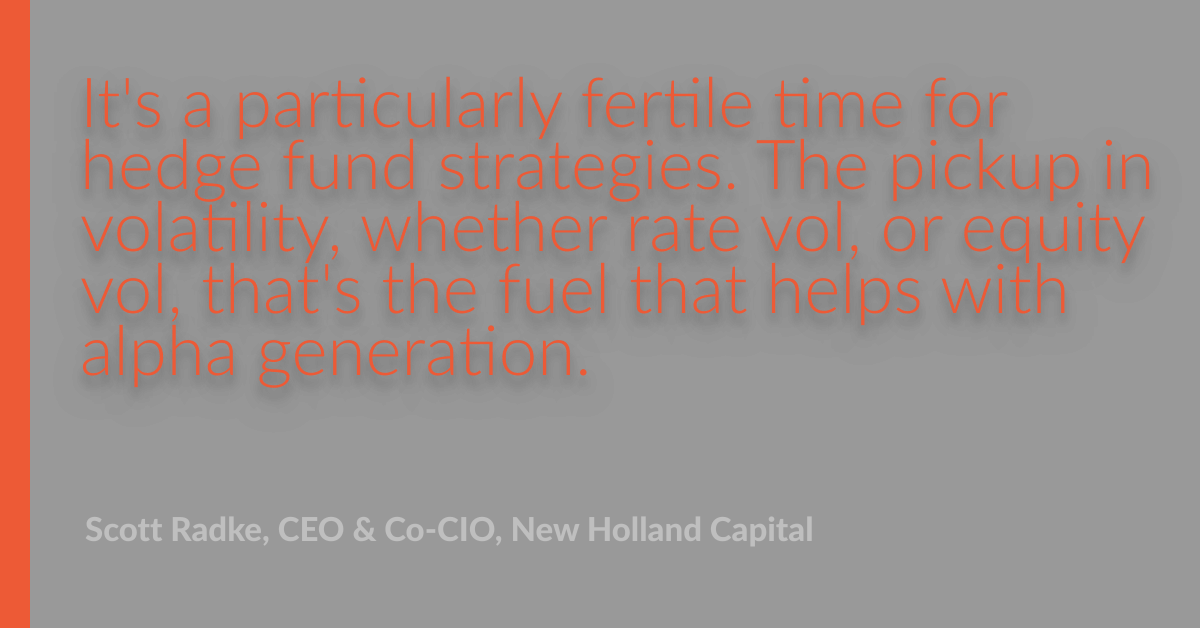

Radke echoes this sentiment but highlights a silver lining: “It’s a particularly fertile time for hedge fund strategies.” Increased volatility across rate, equity, and credit markets provides “the fuel that helps with alpha generation.” Strategies like merger arbitrage, event-driven plays, and commodity-relative value trading are poised to thrive as corporate activity accelerates and historical market relationships are disrupted.

A fertile time for alpha strategies–Why?

Scott Radke shares his insight on why the pickup in volatility and uncertainty provides fertile conditions for hedge fund strategies (alpha-generating strategies).

The Tactical Alpha Edge

At the heart of the conversation was the launch of AGF NHC Tactical Alpha Fund, a multi-strategy approach designed to blend return generation with diversification. Radke emphasizes the importance of assembling a portfolio of strategies that not only deliver returns but also mitigate downside risk in adverse markets.

This fund, described by Radke as a “utility player in baseball,” offers a unique combination of attributes. Its ability to capture upside potential while buffering against downside risk makes it a powerful tool for advisors seeking to stabilize portfolios amidst uncertainty.

“The launch of the fund is also the next step in our partnership with NHC as we continue to build and grow our alternatives business and diversify our capabilities. It is exciting to bring to Canada a product that gives accredited investors access to NHC’s institutional caliber and extensive expertise in absolute return investing,” adds Lawrence.

“It’s not just about generating returns; it’s about doing so in a way that aligns with overarching risk objectives,” Radke explains.

Introducing the AGF NHC Tactical Alpha Strategy

Ash Lawrence describes how the tactical alpha strategy is complementary to traditional portfolio asset allocations in both calm, or stressed, market conditions.

The Blueprint for Success: Multi-Strategy Mastery

Both Lawrence and Radke stress the critical role of manager selection in building resilient portfolios.

Radke’s approach to manager selection blends quantitative rigor with qualitative judgment. “We’re looking for experienced portfolio managers who align philosophically around risk and have a track record of generating exceptional returns,” he says. Beyond the numbers, it’s about identifying partners who demonstrate resilience during challenging market conditions.

“It’s a people business,” Radke notes. “Judging how someone will behave when the chips are down is a different matter entirely.”

What's another way of describing tactical alpha?

Scott Radke eloquently explains 'tactical alpha' in the context what it does for a portfolio.

Radke’s focus on niche, less trafficked strategies has been a hallmark of New Holland Capital’s success. “Crowdedness tends to be a bad characteristic when markets go south,” he explains. By concentrating on a variety of less-crowded esoteric opportunities, Radke’s team has carved out a unique space in the alternatives landscape, enabling their tactical alpha strategy to stand apart from the competition.

How does New Holland Capital stand apart from its competition?

Scott Radke discusses his team's unique approach and the unique space have carved out in the alternatives landscape.

Scott Radke: We've always tended to concentrate on more esoteric strategies, niche investment areas, which sometimes are less scalable.

And that has given us the reputation as the guy to call when you have something that's a little off the beaten path that we're prepared to roll up our sleeves and do the diligence on a less conventional area that's in the belief that there's greater return potential in these less trafficked areas as well as better robustness from a risk perspective.

Crowdedness tends to be a bad characteristic when, when markets go south. So being a little bit to the side of that tends to be beneficial. So that's the other side of it, which is proven to be useful, in that obviously there's a lot of competition for talent, but seeking something that's a bit different than some of our competitors allows us to get different looks than they might.

Lawrence echoes this commitment to specialization, pointing to AGF Capital Partners’ multi-boutique structure as a model for fostering independence while ensuring alignment. “Specialists typically outperform generalists when it comes to alpha generation,” he says. This structure allows AGF Capital Partners to provide its affiliate managers with critical resources—whether distribution networks or quantitative analytics—without compromising their independence.

Education and the Long Game

For Lawrence, educating advisors about the intricacies of alternatives is crucial. “We take a bottoms-up approach, meeting advisors where they are in their knowledge base,” he says. Lawrence acknowledges that there is a wide range of knowledge levels across the advisory landscape. Whether through portfolio modeling or in-depth strategy explanations, AGF Capital Partners’ approach is designed to empower advisors to confidently integrate alternatives into their client portfolios. This involves not only explaining strategies but also modeling their impact on portfolios during both bull and bear markets.

Radke, meanwhile, cautions against the temptation to chase recent performance, urging advisors to differentiate between luck and skill. “The tendency to make trading decisions based on recent returns is the bane of every investor’s existence,” he warns.

How AGF Capital Partners empowers and educates advisors

Ash Lawrence explains how his team works with advisors to empower them to confidently integrate alts in their client portfolios.

Ash Lawrence: There's such a broad range of knowledge, especially within the advisor set.

There are advisors that are very sophisticated. They run very large books. They have analysts that help them, diligence managers, all the way down to an advisor that maybe has no alts exposure at the moment and doesn't have the knowledge. So we tackle it in a couple of different levels.

And what I just said is the first level, just understanding the knowledge base of the advisor that you're speaking to. Depending on that level, we might even take the approach of helping them understand just allocations and what the impacts of certain types of alts within their portfolio might do, including in times of market stress, as well as the good times, to Scott's point about not getting too focused on returns because things don't always go up to the right.

We have a portfolio consulting team here that sometimes we use to help model those things out. Once we have that level of understanding about where they are and how they understand their portfolio, then we can actually get into the various strategies that our team is marketing, whether that's the tactical alpha strategy that Scott and his team run, the private equity strategy that our partners at Kensington run, or our Canadian private credit strategy as well, because we'll have an understanding now of the portfolio. They'll understand how alts work if they didn't already.

Now they can think about what the different features and again, the three I described all have very different features and very different uses within a portfolio. Then we actually get into the education around the underlying strategy and what it means as well as some of the structural trade offs. That's a really important conversation to make sure that the investor understands liquidity.

I think we've seen over the past couple of years, a sort of level of, I'll call it surprise, when certain funds that limited liquidity and certain structural features allowed them to delay or slow down redemptions, and within certain investor sets, they just weren't really aware that that was how these funds worked.

And there are reasons they operate that way – for the protection of investors-both those staying and leaving. But it's really important that they understand that before they go in. It's really important that they understand a lot of these strategies should not come from the part of your portfolio that you might need to be liquid.

The Liquidity Puzzle

The illiquidity premium—often a cornerstone of alternative investing—is another key theme. Lawrence notes that determining the appropriate illiquidity bucket in a portfolio is critical. “You need to decide well in advance how much capital you’re willing to set aside for up to 10 years,” he advises. Radke added that the AGF NHC Tactical Alpha Fund’s focus on public markets allows it to offer some liquidity without sacrificing return potential. “Our structure works in both sunny and rainy markets,” he explains.

How does the AGF NHC Tactical Alpha strategy offer investors the 'best of both worlds' in terms of liquidity?

Scott Radke details how NHC is able to offer investors some liquidity without sacrificing the "illiquidity premium" of their tactical alpha strategy.

Scott Radke: Nearly all of the assets that we manage in the tactical alpha strategy are in public markets that are liquid to varying degrees. So it natively lends itself to being able to offer a liquid fund to investors without having to do 'structuring gymnastics' to make that possible.

Having said that, there's dimensions to that where some of the strategies that we pursue are on the slightly less liquid end because they're more niche and we need to monitor that carefully, and always keep in mind the promises that we've made in terms of the the terms of the vehicles that we manage.

We really orient our investors to think about the allocation to the tactical alpha strategies in particular, in a long term way, in so much as, we know through experience that return production does not happen evenly over time. There are periods that are very difficult to anticipate that just tend to be better, and some where you're working just as hard, but it just feels hard to generate the returns.

And, I think it's a mistake to try to time that, however, we appreciate that conditions change and circumstances warrant people accessing liquidity, so it's important to be able to offer that. And in a way, that's one of the things that differentiates what we do from, say, private equity, which is more natively a long term illiquid private market strategy.

Takeaways

As markets evolve, so too must the tools and strategies advisors use to guide their clients. Here are the key takeaways from the conversation:

- Adapt to New Realities: The post-GFC era of easy equity returns is over. Advisors need to think creatively about diversification and risk management.

- Focus on Manager Selection: Success in alternatives hinges on finding the right people. Look for managers who excel in niche areas and exhibit resilience under pressure.

- Balance Liquidity and Returns: Illiquid investments can provide stability and higher returns, but determining the appropriate allocation is crucial.

- Prioritize Education: Understanding the complexities of alternative strategies is a long-term process. Advisors should leverage the expertise and resources from firms like AGF Capital Partners' to enhance their knowledge.

- Embrace Diversification: Strategies like the AGF NHC Tactical Alpha Fund demonstrate the power of combining return generation with risk mitigation.

Conclusion

In a world of heightened volatility and shifting return dynamics, alternatives are no longer optional—they’re essential. As Lawrence aptly puts it, “We’re here to be your partner in your learning experience.” For advisors willing to invest the time and effort to master these tools, the rewards—both for their clients and their practices—can be substantial.

About Franklin Templeton Investments

Franklin Resources, Inc. [NYSE:BEN] is a global investment management organization with subsidiaries operating as Franklin Templeton and serving clients in over 150 countries. In Canada, the company's subsidiary is Franklin Templeton Investments Corp., which operates as Franklin Templeton Canada. In Canada, Franklin Fixed Income is a business name used by Franklin Templeton Investments Corp. Franklin Templeton's mission is to help clients achieve better outcomes through investment management expertise, wealth management and technology solutions. Through its specialist investment managers, the company offers specialization on a global scale, bringing extensive capabilities in fixed income, equity, alternatives and multi-asset solutions. With more than 1,400 investment professionals, and offices in major financial markets around the world, the California-based company has over 75 years of investment experience and approximately US$1.6 trillion (approximately CAN$2.2 trillion) in assets under management as of July 31, 2025. For more information, please visit franklintempleton.ca.

Important legal information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell, or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager, and the comments, opinions, and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region, or market. Commissions, trailing commissions, management fees, brokerage fees, and expenses may be associated with investments in mutual funds and ETFs. Please read the prospectus and fund fact/ETF facts document before investing. Mutual funds and ETFs are not guaranteed. Their values change frequently. Past performance may not be repeated. Franklin Templeton Canada is a business name used by Franklin Templeton Investments Corp.

Copyright © AdvisorAnalyst.com, Franklin Templeton Investments